On forgetting, Keynes, and the current economy, from Paul Krugman at Voxeu.

Mr Keynes and the moderns

Paul Krugman |

Keynes’ General Theory is 75 years old. In this column, Paul Krugman argues that many of its insights and lessons are still relevant today, but many have been forgotten. A broad swath of macroeconomists and policymakers are applying old fallacies to today’s crisis. As the nostrums being applied by the “pain caucus” are visibly failing, Keynesian ideas may yet make a comeback. It’s a great honour to be asked to give this talk, especially because I’m arguably not qualified to do so.[1] I am, after all, not a Keynes scholar, nor any kind of serious intellectual historian. Nor have I spent most of my career doing macroeconomics. Until the late 1990s my contributions to that field were limited to international issues; although I kept up with macro research, I avoided getting into the frontline theoretical and empirical disputes. By contrast I probably do have a better sense than most technically competent economists of the arguments that actually drive political discourse and policy. And this discourse currently involves many of the same issues Keynes grappled with 75 years ago. We are – frustratingly – retracing much of the same ground covered in the 1930s. The Treasury view is back; liquidationism is once again in full flower. We’re having to relearn the seeming paradox of liquidity-preference versus loanable-funds models of interest rates. What I want to do in this lecture is talk first, briefly, about how to read Keynes – or rather about how I like to read him. I’ll talk next about what Keynes accomplished in The General Theory, and how some current disputes recapitulate old arguments that Keynes actually settled. I’ll follow with a discussion of some crucial aspects of our situation now – and arguably our situation 75 years ago – that are not in the General Theory, or at least barely mentioned. And finally, I’ll reflect on the troubled path that has led us to forget so much of what Keynes taught us. |

On reading Keynes

What did Keynes really intend to be the key message of the General Theory? My answer is, that’s a question for the biographers and the intellectual historians. I won’t quite say I don’t care, but it’s surely not the most important thing. There’s an old story about a museum visitor who examined a portrait of George Washington and asked a guard whether he really looked like that. The guard answered, “That’s the way he looks now.” That’s more or less how I feel about Keynes. What matters is what we make of Keynes, not what he “really” meant.

I’d divide Keynes readers into two types: Chapter 12ers and Book 1ers. Chapter 12 is, of course, the wonderful, brilliant chapter on long-term expectations, with its acute observations on investor psychology, its analogies to beauty contests, and more. Its essential message is that investment decisions must be made in the face of radical uncertainty to which there is no rational answer, and that the conventions men use to pretend that they know what they are doing are subject to occasional drastic revisions, giving rise to economic instability. What Chapter 12ers insist is that this is the real message of Keynes, that all those who have invoked the great man’s name on behalf of quasi-equilibrium models that push this insight into the background – from John Hicks to Paul Samuelson to Mike Woodford – have violated his true legacy.

Part 1ers, by contrast, see Keynesian economics as being essentially about the refutation of Say’s Law – the possibility of a general shortfall in demand. And they generally find it easiest to think about demand failures in terms of quasi-equilibrium models in which some things, including wages and the state of long-term expectations in Keynes’s sense, are held fixed while others adjust toward a conditional equilibrium of sorts. They draw inspiration from Keynes’s exposition of the principle of effective demand in Chapter 3, which is, indeed, stated as a quasi-equilibrium concept: “The value of D at the point of the aggregate demand function, where it is intersected by the aggregate supply function, will be called the effective demand”.

So who’s right about how to read the General Theory? Keynes himself weighed in, in his 1937 QJE article (Keynes 1937), and in effect declared himself a Chapter12er. But so what? Keynes was a great man, but only a man, and our goal now is not to be faithful to his original intentions, but rather to enlist his help in dealing with the world as best we can.

For what it’s worth, I’m basically a Part 1er, with a lot of Chapters 13 and 14 in there too, of which more shortly. Chapter 12 is a wonderful read, and a very useful check on the common tendency of economists to assume that markets are sensible and rational. But what I’m always looking for in economics is ‘intuition pumps’ – ways to think about an economic situation that let you get beyond wordplay and prejudice, that seem to grant some deeper insight. And quasi-equilibrium stories are powerful intuition pumps, in a way that deep thoughts about fundamental uncertainty are not. The trick, always, is not to take your equilibrium stories too seriously, to understand that they’re aids to insight, not Truths; given that, I don’t believe that there’s anything wrong with using equilibrium analysis.

And as it turns out, Keynes-as-equilibrium-theorist – whether or not that’s the “real” Keynes – has a lot to teach us to this day. The struggle to liberate ourselves from Say’s Law, to refute the “Treasury view” and all that, may have seemed like ancient history not long ago, but now that we’re faced with an economic scene reminiscent of the 1930s and we’re having to fight those intellectual battles all over again. And the distinction between loanable funds and liquidity preference theories of the rate of interest – or, rather, the ability to see how both can be true at once, and the implications of that insight – seem to have been utterly forgotten by a large fraction of economists and those commenting on economics.

Old fallacies in new battles

When you read dismissals of Keynes by economists who don’t get what he was all about – which means many of our colleagues – you fairly often hear his contribution minimised as amounting to no more than the notion that wages are sticky, so that fluctuations in nominal demand affect real output. Here’s Robert Barro (2009): “John Maynard Keynes thought that the problem lay with wages and prices that were stuck at excessive levels. But this problem could be readily fixed by expansionary monetary policy, enough of which will mean that wages and prices do not have to fall.”And if that’s all that it was about, the General Theory would have been no big deal.

But of course, it wasn’t just about that. Keynes’s critique of the classical economists was that they had failed to grasp how everything changes when you allow for the fact that output may be demand-constrained. They mistook accounting identities for causal relationships, believing in particular that because spending must equal income, supply creates its own demand and desired savings are automatically invested. And they had a theory of interest that thought solely in terms of the supply and demand for funds, failing to realise that savings in particular depend on the level of income, and that once you take this into account you need something else – liquidity preference – to complete the story.

I know that there’s dispute about whether Keynes was fair in characterizing the classical economists in this way. But I’m inclined to believe that he was right. Why? Because you can see modern economists and economic commentators who don’t know their Keynes falling into the very same fallacies.

There’s no way for me to make this point without citing specific examples, which means naming names. So, on the first point, here’s Chicago’s John Cochrane (2009):

“First, if money is not going to be printed, it has to come from somewhere. If the government borrows a dollar from you, that is a dollar that you do not spend, or that you do not lend to a company to spend on new investment. Every dollar of increased government spending must correspond to one less dollar of private spending. Jobs created by stimulus spending are offset by jobs lost from the decline in private spending. We can build roads instead of factories, but fiscal stimulus can’t help us to build more of both. This is just accounting, and does not need a complex argument about “crowding out.””

That’s precisely the position Keynes attributed to classical economists – “the notion that if people do not spend their money in one way they will spend it in another.” And as Keynes said, this misguided notion derives its plausibility from its superficial resemblance to the accounting identity which says that total spending must equal total income.

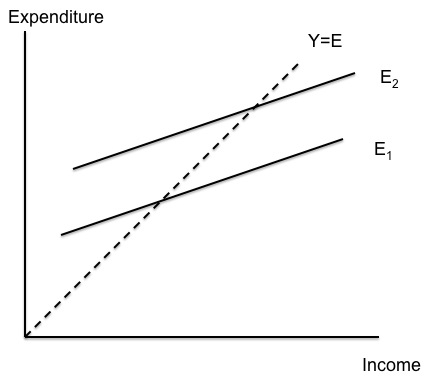

All it takes to dispel this fallacy is the hoary old Samuelson cross (Figure 1), in which the schedules E1 and E2 represent desired spending as a function of income. Equilibrium – or, if you like, quasi-equilibrium – is at the point where the spending schedule crosses the 45-degree line, so spending does equal income. But this accounting identity by no means implies that an increase in desired spending, whether by the government or a private actor, cannot affect actual spending. Yes, I said a private actor. As some of us have pointed out, the argument that deficit spending by the government cannot raise income also implies that a decision by a private business to spend more must crowd out an equal amount of spending elsewhere in the economy. Needless to say, in the political debate this point isn’t appreciated; conservatives tend to insist both that fiscal policy can’t work and that improving business confidence is crucial. But that’s politics.

Figure 1.

On the contrary, as the Samuelson cross shows, a rise in desired spending will normally translate into a rise in income.

But you can see right away part of our problem. Who teaches the Samuelson cross these days? In particular, who teaches it in graduate school? It’s regarded as too crude, too old-fashioned to be even worth mentioning. Yet it conveys a basic point that is more sophisticated than what a lot of reputable economists are saying – in fact, if they had ever learned this crude construct it would have saved them from falling into a naïve fallacy. And while it’s possible to convey the same point in terms of more elaborate New Keynesian models, such models, by their very complexity, fail to make the point as forcefully as the good old 45-degree diagram.

What about interest rates?

Keynes’s discussion of interest rate determination in Chapter 13 and 14 of the General Theory is much more profound than, I think, most readers realise (perhaps because it’s also rather badly written). The proof of its profundity lies in the way so many people – including highly reputable economists – keep falling into the fallacies Keynes laid out, both in discussions of fiscal policy and in discussions of international capital flows.

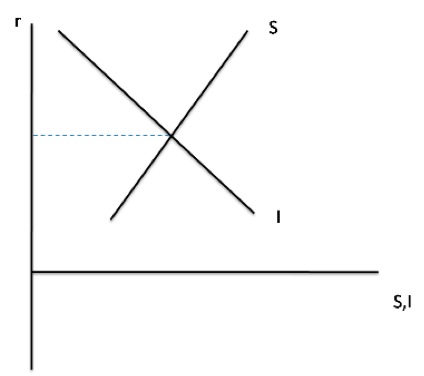

Figure 2.

The natural inclination of practical men – who are not necessarily slaves of defunct economists since there are plenty of live and kicking economists ready to aid and abet their misconceptions – is to think of the interest rate as being determined by the supply and demand for loanable funds, as in Figure 2. When you think in those terms, it’s only natural to suppose that any increase in the demand for or fall in the supply of loanable funds must drive up interest rates; and it’s easy to imagine that this, in turn, would hurt prospects for economic recovery.

Again, I need to name names to assure you that I’m not inventing straw men. So here’s Niall Ferguson (in Soros et al 2009):

“Now we’re in the therapy phase. And what therapy are we using? Well, it’s very interesting because we’re using two quite contradictory courses of therapy. One is the prescription of Dr Friedman – Friedman, that is – which is being administered by the Federal Reserve: massive injections of liquidity to avert the kind of banking crisis that caused the Great Depression of the early 1930s. I’m fine with that. That’s the right thing to do. But there is another course of therapy that is simultaneously being administered, which is the therapy prescribed by Dr Keynes – John Maynard Keynes—and that therapy involves the running of massive fiscal deficits in excess of 12% of gross domestic product this year, and the issuance therefore of vast quantities of freshly minted bonds.

“There is a clear contradiction between these two policies, and we’re trying to have it both ways. You can’t be a monetarist and a Keynesian simultaneously – at least I can’t see how you can, because if the aim of the monetarist policy is to keep interest rates down, to keep liquidity high, the effect of the Keynesian policy must be to drive interest rates up.

“After all, $1.75 trillion is an awful lot of freshly minted treasuries to land on the bond market at a time of recession, and I still don’t quite know who is going to buy them. It’s certainly not going to be the Chinese. That worked fine in the good times, but what I call “Chimerica”, the marriage between China and America, is coming to an end. Maybe it’s going to end in a messy divorce.”

What’s wrong with this line of reasoning? It’s exactly the logical hole Keynes pointed out, namely that the schedules showing the supply and demand for funds can only be drawn on the assumption of a given level of income. Allow for the possibility of a rise in income, and you get Figure 3 – which is Keynes’s own figure, and a horrible drawing it is.

Figure 3.

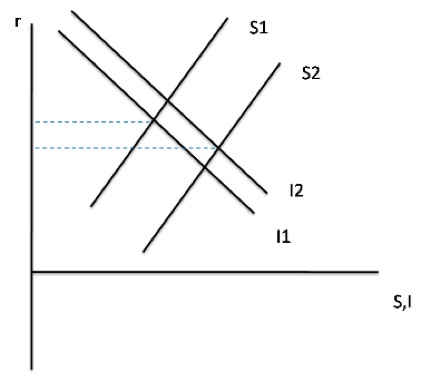

Figure 4 is my own version, very much along Hicks’s lines: we imagine that a rise in GDP shifts the savings schedule out from S1 to S2, also shifts the investment schedule, and, as drawn, reduces the equilibrium interest rate in the market for loanable funds.

Figure 4.

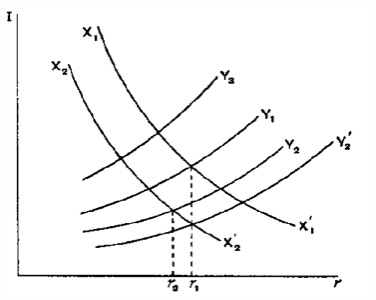

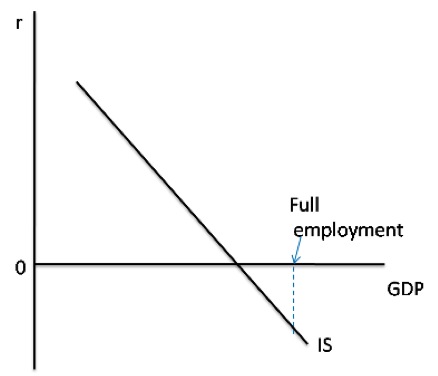

As Hicks told us – and as Keynes himself says in Chapter 14 – what the supply and demand for funds really give us is a schedule telling us what the level of income will be for a given rate of interest. That is, it gives us the IS curve of Figure 5; this tells us where the central bank must set the interest rate so as to achieve a given level of output and employment. Of course, as the figure indicates, it’s possible that the interest rate required to achieve full employment is negative, in which case monetary policy is up against the zero lower bound, that is, we’re in a liquidity trap. That’s where America and Britain were in the 1930s – and we’re back there again.

Figure 5.

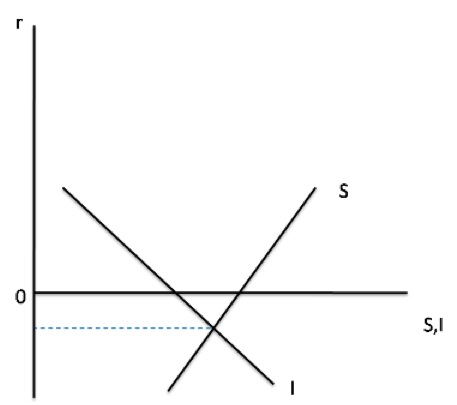

One way to think about this situation is to draw the supply and demand for loanable funds that would prevail if we were at full employment, as in Figure 6. The point then is that there’s an excess supply of desired savings at the zero interest rate that’s the lowest achievable. A zero-lower-bound economy is, fundamentally, an economy suffering from an excess of desired saving over desired investment.

Which brings me back to the argument that government borrowing under current conditions will drive up interest rates and impede recovery. What anyone who understood Keynes should realise is that as long as output is depressed, there is no reason increased government borrowing need drive rates up; it’s just making use of some of those excess potential savings – and it therefore helps the economy recover. To be sure, sufficiently large government borrowing could use up all the excess savings, and push rates up – but to do that the government borrowing would have to be large enough to restore full employment!

Figure 6.

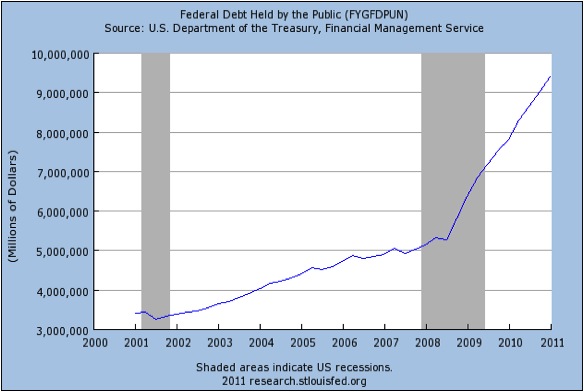

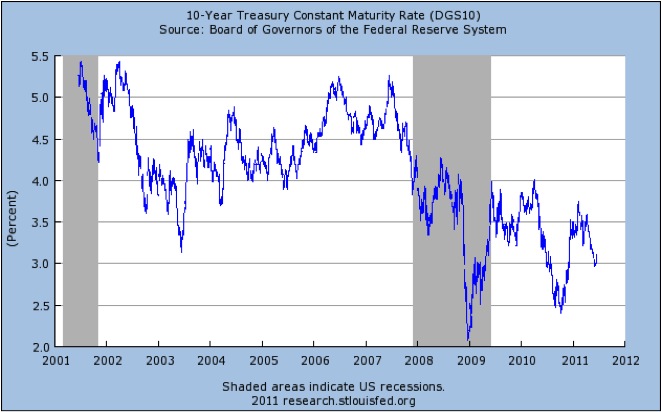

But what of those who cling to the view that government borrowing must drive up rates, never mind all this hocus-pocus? Well, we’ve has as close to a controlled experiment as you ever get in macroeconomics. Figure 7 shows U.S. federal debt held by the public, which has risen around $4 trillion since the economy entered liquidity-trap conditions. And Figure 8 shows 10-year interest rates, which have actually declined. (Long rates aren’t zero because the market expects the Fed funds rate to rise at some point, although that date keeps being pushed further into the future.)

Figure 7.

Figure 8.

So those who were absolutely certain that large borrowing would push up interest rates even in the face of a depressed economy fell into the very fallacy Keynes went to great lengths to refute. And once again, I’ve made that point using very old-fashioned analysis – the kind of analysis many economist no longer learn. New Keynesian models, properly understood, could with greater difficulty get you to the same result. But how many people properly understand these models?

I’m not quite done here. If much of our public debate over fiscal policy has involved reinventing the same fallacies Keynes refuted in 1936, the same can be said of debates over international financial policy. Consider the claim, made by almost everyone, that given its large budget deficits the US desperately needs continuing inflows of capital from China and other emerging markets. Even very good economists fall into this trap. Just last week Ken Rogoff declared that “loans from emerging economies are keeping the debt-challenged US economy on life support.”

Um, no: inflows of capital from other nations simply add to the already excessive supply of U.S. savings relative to investment demand. These inflows of capital have as their counterpart a trade deficit that makes America worse off, not better off; if the Chinese, in a huff, stopped buying Treasuries they would be doing us a favour. And the fact that top officials and highly regarded economists don’t get this, 75 years after the General Theory, represents a sad case of intellectual regression.

I’ll have more to say about that intellectual regression later. But first let’s talk about key features of our current situation that aren’t in Keynes.

What wasn’t in the General Theory: Banks and debt

Perhaps the most surprising omission in the General Theory – and the one that has so far generated the most soul-searching among those macroeconomists who had not forgotten basic Keynesian concepts – is the book’s failure to discuss banking crises. There’s basically no financial sector in the General Theory; textbook macroeconomics ever since has more or less discussed money and banking off to the side, giving it no central role in business cycle analysis.

I’d be curious to hear what Keynes scholars have to say about this omission. Keynes was certainly aware of the possibility of banking problems; his 1931 essay “The Consequences to the Banks of the Collapse of Money Values” is a razor-sharp analysis of just how deflation could produce a banking crisis, as indeed it did in the US.

But not in Britain, which may be one reason Keynes left the subject out of the General Theory. Beyond that, Keynes was – or at least that’s how it seems to a Part 1er – primarily concerned with freeing minds from Say’s Law and the notion that, if there was any demand problem, it could be solved simply by increasing the money supply. A prolonged focus on banking issues could have distracted from that central point. Indeed, I would argue that something very like that kind of distraction occurred in economic discussion of Japan in the 1990s. All too many analyses focused on zombie banks and all that, and too few people realised that Japan’s liquidity trap was both more fundamental and more ominous in its implications for economic policy elsewhere than one would recognise if it was diagnosed solely as a banking problem.

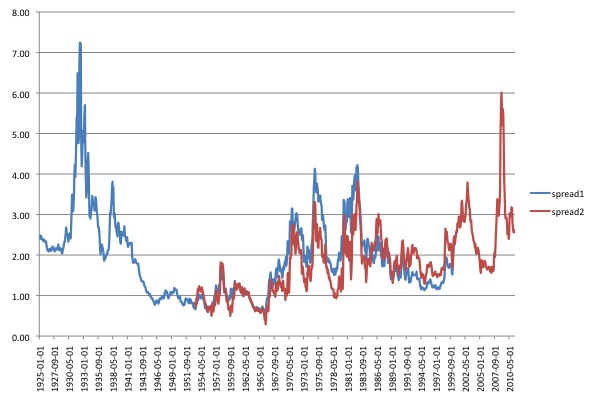

This time around, of course, there was no mistaking the crucial role of the financial sector in creating a terrifying economic crisis. You can use any of a number of indicators of financial stress to track the recent crisis. In Figure 9 I use the spread between Baa-rated corporate debt and long-term federal debt (“spread1” is against the long-term rate on federal debt, “spread2” against the 10-year constant maturity Treasury yield), which has the advantage both of being a measure one can track over a very long history and of being a measure stressed by a fellow named Ben Bernanke in his analyses of the onset of the Great Depression. As you can see, there have been two great financial disruptions in modern American history, the first associated with the banking crisis of 1930-31, the second with the shadow banking crisis of 2008.

Figure 9.

Nobody can doubt that these financial crises played a key role in the onset both of the Great Depression and of our recent travails, which Brad DeLong has taken to calling the Little Depression. And yet I am increasingly convinced that it’s a mistake to think of our problems as being entirely or even mainly a financial-sector issue. As you can see from Figure 9 the financial disruptions of 2008 and early 2009 have largely gone away. Yet while the economy’s freefall has ended, we’ve hardly had a full recovery. Something else must be holding the economy down.

Like many others, I’ve turned to debt levels as a key part of the story – specifically, the surge in household debt that began in the early 1980s, accelerated drastically after 2002, and finally went into reverse after the financial crisis struck.

In recent work I’ve done with Gauti Eggertsson (Eggertsson and Krugman 2010), we’ve tried to put debt into a New Keynesian framework. The key insight is that while debt does not make the world poorer – one person’s liability is another person’s asset – it can be a source of contractionary pressure if there’s an abrupt tightening of credit standards, i.e. if levels of leverage that were considered acceptable in the past are suddenly deemed unacceptable thanks to some kind of shock such as, well, a financial crisis. In that case debtors are faced with the necessity of deleveraging. This forces them to slash spending while creditors face no comparable need to spend more. Such a situation can push an economy up against the zero lower-bound and keep it there for an extended period.

I can’t quite find this story in the General Theory, although the idea of a sudden revision of conventional views about how much debt is safe certainly fits the spirit of Chapter 12. In any case, however, Keynes was definitely aware of the implications of debt and the constraints it puts on debtors for other macroeconomic questions. In the General Theory – and in reality – debt is a crucial reason why the notion expressed by Barro – that it’s just about nominal wages being too high – not only misses the point but even gets the direction of effect wrong.

In textbook macroeconomics we draw a downward-sloping aggregate demand curve, and in that framework it does look as if a fall in nominal wages, which shifts the aggregate supply curve down, would raise employment. The argument for expansionary policy is then one of practicality: it’s easier to push AD up using monetary policy than to push wages down. Indeed, in simple post-Keynesian models it does all boil down to M/w, the ratio of the money supply to the wage rate.

But this presupposes, first, that a rise in the real quantity of money is actually expansionary, which is normally true, but highly dubious if an economy is up against the zero lower bound. If changes in M/P don’t matter, then the aggregate demand curve becomes vertical – or worse.

For if there are spending-constrained debtors with debts specified in nominal terms – as there are in today’s world – a fall in wages, leading to a fall in the general price level, worsens the real burden of debt and actually has a contractionary effect on the economy. This is a point of which Keynes was well aware, although it got largely lost even in the relatively Keynesian literature of the 40s and 50s.

When does the need for deficit spending end?

There’s something else worth pointing out about an analysis that stresses the role of debtors forced into rapid deleveraging. It helps solve a problem Keynes never addressed, namely, when does the need for deficit spending end?

The reason this is relevant is concern about rising public debt. I constantly encounter the argument that our crisis was brought on by too much debt – which is largely my view as well – followed by the insistence that the solution can’t possibly involve even more debt.

Once you think about this argument, however, you realise that it implicitly assumes that debt is debt – that it doesn’t matter who owes the money. Yet that can’t be right; if it were, we wouldn’t have a problem in the first place. After all, the overall level of debt makes no difference to aggregate net worth – one person’s liability is another person’s asset.

It follows that the level of debt matters only if the distribution of net worth matters, if highly indebted players face different constraints from players with low debt. And this means that all debt isn’t created equal – which is why borrowing by some actors now can help cure problems created by excess borrowing by other actors in the past.

Suppose, in particular, that the government can borrow for a while, using the borrowed money to buy useful things like infrastructure. The true social cost of these things will be very low, because the spending will be putting resources that would otherwise be unemployed to work. And government spending will also make it easier for highly indebted players to pay down their debt. If the spending is sufficiently sustained, it can bring the debtors to the point where they’re no longer so severely balance-sheet constrained, and further deficit spending is no longer required to achieve full employment.

Yes, private debt will in part have been replaced by public debt – but the point is that debt will have been shifted away from severely balance-sheet-constrained players, so that the economy’s problems will have been reduced even if the overall level of debt hasn’t fallen.

The bottom line, then, is that the plausible-sounding argument that debt can’t cure debt is just wrong. On the contrary, it can – and the alternative is a prolonged period of economic weakness that actually makes the debt problem harder to resolve.

And it seems to me that thinking explicitly about the role of debt, not just with regard to the usefulness or lack thereof of wage flexibility, but as a key causal factor behind slumps, improves Keynes’s argument. In the long run we are, indeed, all dead, but it’s helpful to have a story about why expansionary fiscal policy need not be maintained forever.

The strange death of Keynesian policy: Instability of the Samuelsonian synthesis

So far I’ve argued that Keynesian analysis – or at least what Keynesian analysis looks like now, whatever Keynes may “really” have meant – is an excellent tool for understanding the mess we’re in. Where simple Keynesian models seem to conflict with common sense, with the wisdom of practical men, the Keynesian models are right and the wisdom of the practical men entirely wrong.

So why are we making so little use of Keynesian insights now that we’re living in an economy that, in many respects, resembles the economy of the 1930s? Why are we having to have the old arguments all over again? For it does seem as if all the old fallacies are new again.

By all means let us condemn famous men. There is no excuse for the timidity of Barack Obama, the wishful thinking of Jean-Claude Trichet, and the determined ignorance of almost everyone in the Republican Party. But watching the failure of policy over the past three years, I find myself believing, more and more, that this failure has deep roots – that we were in some sense doomed to go through this. Specifically, I now suspect that the kind of moderate economic policy regime economists in general used to support – a regime that by and large lets markets work, but in which the government is ready both to rein in excesses and fight slumps – is inherently unstable. It’s something that can last for a generation or so, but not much longer.

By “unstable” I don’t just mean Minsky-type financial instability, although that’s part of it. Equally crucial are the regime’s intellectual and political instability.

Let me start with the intellectual instability.

The brand of economics I use in my daily work – the brand that I still consider by far the most reasonable approach out there – was largely established by Paul Samuelson back in 1948, when he published the first edition of his classic textbook. It’s an approach that combines the grand tradition of microeconomics, with its emphasis on how the invisible hand leads to generally desirable outcomes, with Keynesian macroeconomics, which emphasises the way the economy can develop what Keynes called “magneto trouble”, requiring policy intervention. In the Samuelsonian synthesis, one must count on the government to ensure more or less full employment; only once that can be taken as given do the usual virtues of free markets come to the fore.

It’s a deeply reasonable approach – but it’s also intellectually unstable. For it requires some strategic inconsistency in how you think about the economy. When you’re doing micro, you assume rational individuals and rapidly clearing markets; when you’re doing macro, frictions and ad hoc behavioural assumptions are essential.

So what? Inconsistency in the pursuit of useful guidance is no vice. The map is not the territory, and it’s OK to use different kinds of maps depending on what you’re trying to accomplish. If you’re driving, a road map suffices. If you’re going hiking, you really need a topographic survey.

But economists were bound to push at the dividing line between micro and macro – which in practice has meant trying to make macro more like micro, basing more and more of it on optimisation and market-clearing. And if the attempts to provide “microfoundations” fell short? Well, given human propensities, plus the law of diminishing disciples, it was probably inevitable that a substantial part of the economics profession would simply assume away the realities of the business cycle, because they didn’t fit the models.

The result was what I’ve called the Dark Age of macroeconomics, in which large numbers of economists literally knew nothing of the hard-won insights of the 30s and 40s – and, of course, went into spasms of rage when their ignorance was pointed out.

To this intellectual instability, add political instability.

It’s possible to be both a conservative and a Keynesian; after all, Keynes himself described his work as “moderately conservative in its implications.” But in practice, conservatives have always tended to view the assertion that government has any useful role in the economy as the thin edge of a socialist wedge. When William Buckley wrote God and Man at Yale, one of his key complaints was that the Yale faculty taught – horrors! – Keynesian economics.

I’ve always considered monetarism to be, in effect, an attempt to assuage conservative political prejudices without denying macroeconomic realities. What Friedman was saying was, in effect, yes, we need policy to stabilise the economy – but we can make that policy technical and largely mechanical, we can cordon it off from everything else. Just tell the central bank to stabilise M2, and aside from that, let freedom ring!

When monetarism failed – fighting words, but you know, it really did — it was replaced by the cult of the independent central bank. Put a bunch of bankerly men in charge of the monetary base, insulate them from political pressure, and let them deal with the business cycle; meanwhile, everything else can be conducted on free-market principles.

And this worked for a while – roughly speaking from 1985 to 2007, the era of the Great Moderation. It worked in part because the political insulation of central banks also gave them more than a bit of intellectual insulation, too. If we’re living in a Dark Age of macroeconomics, central banks have been its monasteries, hoarding and studying the ancient texts lost to the rest of the world. Even as the real business cycle people took over the professional journals, to the point where it became very hard to publish models in which monetary policy, let alone fiscal policy, matters, the research departments of the Fed system continued to study counter-cyclical policy in a relatively realistic way.

But this, too, was unstable. For one thing, there was bound to be a shock, sooner or later, too big for the central bankers to handle without help from broader fiscal policy. Also, sooner or later the barbarians were going to go after the monasteries too; and as the current furore over quantitative easing shows, the invading hordes have arrived.

Last but not least, there is financial instability. As I see it, the very success of central-bank-led stabilization, combined with financial deregulation – itself a by-product of the revival of free-market fundamentalism – set the stage for a crisis too big for the central bankers to handle. This is Minskyism: the long period of relative stability led to greater risk-taking, greater leverage, and, finally, a huge deleveraging shock. And Milton Friedman was wrong: in the face of a really big shock, which pushes the economy into a liquidity trap, the central bank can’t prevent a depression.

And by the time that big shock arrived, the descent into an intellectual Dark Age combined with the rejection of policy activism on political grounds had left us unable to agree on a wider response.

So the era of the Samuelsonian synthesis was, I suspect, doomed to come to a nasty end. And the result is the wreckage we see all around us.

Dangerous Ideas

The General Theory famously ends with a stirring ode to the power of ideas, which, Keynes asserted, are “dangerous for good or evil.” Generations of economists have taken that ringing conclusion as justification for believing that their work matters – that good ideas will eventually translate into good policy. But how much of that hope can survive now, when both policy makers and many of our colleagues have fallen right back into the fallacies that Keynes exposed?

The best answer I can give is that steady upward progress was probably too much to expect, especially in a field where interests and prejudices run as strong as they do in economics. And there may yet be scope for Keynesian ideas even in the current crisis; after all, the crisis shows no sign of ending soon, and the policies of what I call the pain caucus are visibly failing as we speak. There may be another chance to return to the ideas that should have been governing policy all along.

So since I’m in England, here’s my advice to economists (and policy makers) frustrated – as I am – by the inadequacy of policy responses and the intellectual regression of too much of our profession: Keep calm and carry on. History will vindicate your persistence.

References

Barro, Robert (2009), “Government spending is no free lunch”, Wall Street Journal, January 22.

Cochrane, John (2009), “Fiscal stimulus, fiscal inflation, or fiscal fallacies?”, mimeo.

Eggertsson and Krugman (2010), “Debt, deleveraging, and the liquidity trap”, mimeo.

Keynes, J.M. (1936). The General Theory of Employment, Interest, and Money. New York: Harcourt, Brace and Company.

Keynes, J.M. (1937), “The general theory of employment”, Quarterly Journal of Economics.

George Soros, Niall Ferguson, Paul Krugman, Robin Wells, and Bill Bradley, et al. (2009), “The crisis and how to deal with it”, New York Review of Books, June 11.

[1] Prepared for the Cambridge conference commemorating the 75th anniversary of the publication of The General Theory of Employment, Interest, and Money.

Nenhum comentário:

Postar um comentário